Knowledge Center

Asset Allocation and Why You Need to Rebalance

Allocating Your Investments

Every dollar you put toward your retirement is another step towards a more secure financial future. And you control how much of your contributions go to more than a dozen self-directed and objective-based funds that RPB offers.

To help you decide how you want to allocate your savings—also known as asset allocation—ask yourself the following questions:

- When do I want to retire? While many people expect to retire at 65, some try to put more money aside so they can retire earlier. Others might want to keep working beyond that. It’s all based on your personal situation.

- How much money will I need when I stop working? Although it may seem hard to predict how much money you’ll need to retire, think about where you might want to live, your expected lifestyle, your health, how long you may live, and how much money you may want to leave to your loved ones.

- What’s my tolerance for risk? You should expect to go through several market cycles while you’re building your nest egg. Some investors may not mind seeing their assets rise and fall with the markets, while others might not want to put their savings at risk in a downward cycle. Your ability to tolerate volatile markets is a key factor in determining where to invest your retirement savings.

Your investment objectives will likely change as you get older or reach life milestones such as a marriage or the birth of a child. If you’re working and contributing for a few decades, you may opt to invest in more aggressive funds that can weather market fluctuations over time. Or maybe you’re in a later stage of your career, and you want to invest in a more conservative fund that’s more insulated against losses.

Good to Know:

It’s best to review your asset allocations annually to ensure that your fund elections still match your retirement goals and expectations.

You also have the flexibility to invest your current savings in different funds than your future contributions. For example, a participant with assets currently invested in a growth fund may want to maintain that asset allocation and direct all future contributions into a more conservative fund.

Rebalancing Your Portfolio

But no matter how you allocate your investments, over time the unpredictable nature of the markets is probably going to affect your fund allocations. That’s why you want to rebalance your assets to keep them in line with your objectives.

When you rebalance or realign your portfolio, you’re not cashing out any assets. Instead, behind the scenes you’re selling assets that have become “overweighted” in your portfolio and using the money to buy into funds that have become “underweighted.”

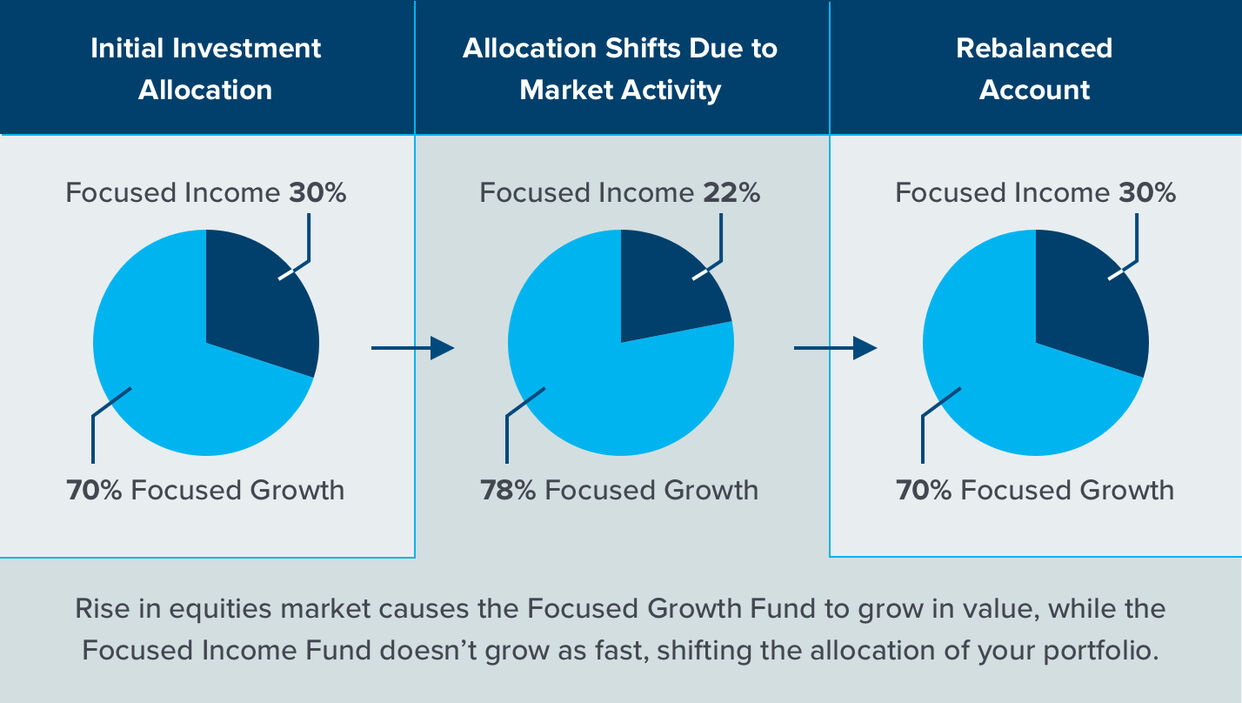

In this hypothetical example, you have $10,000 invested in your retirement account and you decide to split it into two buckets to keep your assets diversified. You have $7,000 in the RPB Focused Growth Fund—which is more aggressive—and $3,000 in the RPB Focused Income Fund, which invests in more stable financial instruments.

One year later, your total investments have grown, but at different rates due to market conditions. You now have 78% of your assets in the RPB Focused Growth Fund, and 22% in the RPB Focused Income Fund. Now, more of your assets are in a riskier asset allocation than the 70% you planned for.

In this case, rebalancing will automatically realign your portfolio to your original objectives by selling 8% of your shares in the RPB Focused Growth Fund to buy more shares in the RPB Focused Income Fund—returning your ownership to 70% and 30%, respectively and ensuring that you’re not taking on more risk than you’re comfortable with.

Good to Know:

Financial professionals generally recommend that you rebalance your portfolio quarterly to ensure that you’re maintaining your desired asset allocation.

Want to learn more about the concept of account rebalancing? Visit this link to read more.